All Categories

Featured

Table of Contents

Area 691(c)( 1) provides that an individual that consists of a quantity of IRD in gross revenue under 691(a) is permitted as a reduction, for the very same taxed year, a part of the inheritance tax paid because the inclusion of that IRD in the decedent's gross estate. Normally, the amount of the reduction is calculated using estate tax worths, and is the quantity that births the very same proportion to the estate tax attributable to the net worth of all IRD items consisted of in the decedent's gross estate as the worth of the IRD consisted of in that individual's gross revenue for that taxable year births to the value of all IRD products consisted of in the decedent's gross estate.

Rev. Rul., 1979-2 C.B. 292, addresses a scenario in which the owner-annuitant acquisitions a deferred variable annuity contract that gives that if the proprietor dies prior to the annuity beginning day, the called recipient may choose to obtain the present built up value of the contract either in the form of an annuity or a lump-sum settlement.

Rul. If the beneficiary chooses a lump-sum repayment, the excess of the quantity received over the quantity of consideration paid by the decedent is includable in the beneficiary's gross earnings.

Rul. Had the owner-annuitant surrendered the agreement and obtained the quantities in excess of the owner-annuitant's financial investment in the agreement, those amounts would have been revenue to the owner-annuitant under 72(e).

Annuity Income Stream inheritance and taxes explained

Likewise, in the existing case, had A surrendered the agreement and got the amounts at concern, those amounts would certainly have been income to A under 72(e) to the level they surpassed A's financial investment in the agreement. As necessary, amounts that B obtains that go beyond A's financial investment in the agreement are IRD under 691(a).

, those amounts are includible in B's gross income and B does not get a basis adjustment in the agreement. B will certainly be qualified to a deduction under 691(c) if estate tax obligation was due by factor of A's death.

DRAFTING Info The major author of this earnings judgment is Bradford R.

Tax consequences of inheriting a Annuity Beneficiary

Q. How are exactly how taxed as tired inheritance? Is there a distinction if I inherit it straight or if it goes to a trust for which I'm the beneficiary? This is a fantastic question, but it's the kind you need to take to an estate planning attorney who knows the details of your scenario.

As an example, what is the partnership between the departed proprietor of the annuity and you, the recipient? What type of annuity is this? Are you making inquiries around revenue, estate or inheritance taxes? After that we have your curveball inquiry concerning whether the result is any kind of different if the inheritance is through a depend on or outright.

We'll think the annuity is a non-qualified annuity, which suggests it's not component of an IRA or other competent retirement plan. Botwinick claimed this annuity would be added to the taxed estate for New Jersey and federal estate tax obligation purposes at its day of fatality value.

Tax on Annuity Payouts death benefits for beneficiaries

person spouse exceeds $2 million. This is referred to as the exemption.Any amount passing to an U.S. resident partner will be totally exempt from New Jacket inheritance tax, and if the proprietor of the annuity lives throughout of 2017, after that there will be no New Jacket estate tax on any amount since the estate tax obligation is set up for repeal starting on Jan. After that there are federal inheritance tax.

The current exemption is $5.49 million, and Botwinick said this tax is possibly not going away in 2018 unless there is some major tax obligation reform in a genuine hurry. Fresh Jacket, federal inheritance tax law offers a complete exemption to amounts passing to making it through U.S. Next, New Jersey's inheritance tax.Though the New Jersey estate tax is scheduled

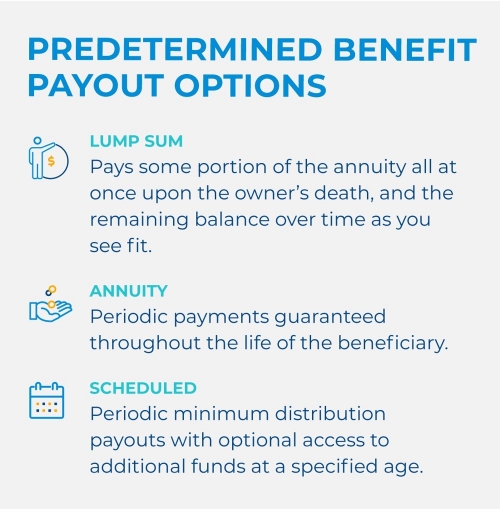

to be repealed in 2018, there is noabolition scheduled for the New Jersey estate tax, Botwinick said. There is no federal inheritance tax obligation. The state tax gets on transfers to everybody besides a particular course of individuals, he claimed. These consist of partners, kids, grandchildren, parent and step-children." The New Jersey estate tax applies to annuities simply as it uses to other assets,"he claimed."Though life insurance payable to a details beneficiary is excluded from New Jersey's inheritance tax, the exemption does not use to annuities. "Currently, income taxes.Again, we're presuming this annuity is a non-qualified annuity." In a nutshell, the earnings are tired as they are paid out. A part of the payment will certainly be dealt with as a nontaxable return of investment, and the incomes will certainly be tired as normal revenue."Unlike acquiring other properties, Botwinick stated, there is no stepped-up basis for acquired annuities. Nonetheless, if inheritance tax are paid as an outcome of the addition of the annuity in the taxable estate, the recipient may be entitled to a deduction for inherited revenue in regard of a decedent, he claimed. Annuity repayments consist of a return of principalthe cash the annuitant pays right into the contractand rate of interestgained inside the contract. The interest section is exhausted as common revenue, while the primary quantity is not tired. For annuities paying out over a much more extensive duration or life span, the principal section is smaller, leading to fewer tax obligations on the monthly payments. For a wedded pair, the annuity agreement may be structured as joint and survivor so that, if one spouse passes away , the survivor will certainly remain to get surefire payments and take pleasure in the very same tax obligation deferral. If a recipient is called, such as the pair's children, they end up being the recipient of an inherited annuity. Recipients have numerous alternatives to consider when choosing how to get money from an acquired annuity.

{kind=link}

Table of Contents

Latest Posts

Decoding Fixed Interest Annuity Vs Variable Investment Annuity A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Features of Fixed Annuity Or Variable Annuity Why Choosin

Exploring the Basics of Retirement Options Key Insights on Your Financial Future What Is the Best Retirement Option? Benefits of Fixed Vs Variable Annuity Pros Cons Why Choosing the Right Financial St

Decoding How Investment Plans Work A Comprehensive Guide to Indexed Annuity Vs Fixed Annuity Defining Fixed Vs Variable Annuity Features of Smart Investment Choices Why Choosing the Right Financial St

More

Latest Posts